MONEY MARKET FUNDS

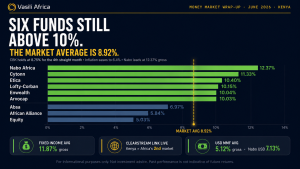

In the month of June 2023, Etica Money Market Fund was the best performing MMF with an average Effective Annual Yield of 11.17%. In second and third position were Cytonn Money Market Fund and Apollo Money Market Fund respectively, recording average Effective Annual Yields of 11.09% and 10.92%.

| FUND MANAGER | MONEY MARKET FUND | ANNUAL YIELD % | |

| 1 | Etica Capital Limited | Etica Money Market Fund | 11.17 |

| 2 | Cytonn Asset Managers Limited | Cytonn Money Market Fund | 11.09 |

| 3 | Apollo Asset Management Company Limited | Apollo Money Market Fund | 10.92 |

| 4 | Enwealth Financial Services | Enwealth Money Market Fund | 10.62 |

| 5 | Madison Investment Managers Limited | Madison Money Market Fund | 10.37 |

| 6 | Jubilee Financial Services Limited | Jubilee Money Market Fund | 10.25 |

| 7 | GenAfrica Asset Managers Limited | GenAfrica Money Market Fund | 10.23 |

| 8 | Kuza Asset Management Limited | Kuza Money Market Fund (KES) | 10.16 |

| 9 | African Alliance | African Alliance Kenya Money Market Fund | 10.09 |

| 10 | Co-op Trust Investment Services Limited | Co-op Money Market Fund | 9.95 |

| 11 | Old Mutual Investment Group | Old Mutual Money Market Fund | 9.88 |

| 12 | KCB Group | KCB Money Market Fund | 9.73 |

| 13 | Sanlam Investments East Africa Limited | Sanlam Money Market Fund | 9.68 |

| 14 | Zimele Asset Management | Zimele Money Market Fund | 9.56 |

| 15 | Nabo Capital Limited | Nabo Africa Money Market Fund | 9.55 |

FIXED-INCOME SECURITIES – TREASURY BILLS

WEEK 1 – 05/06/2023

T-bills were oversubscribed recording an increased overall subscription rate of 98.19% from 91.87% recorded in the previous week.

WEEK 2 – 12/06/2023

T-bills were oversubscribed recording an increased overall subscription rate of 137.95% from 98.19% recorded in the previous week.

WEEK 3 – 19/06/2023

T-bills were undersubscribed recording an overall decreased subscription rate of 94.18% from 137.95% recorded in the previous week.

WEEK 4 – 26/06/2023

T-bills were undersubscribed for the second week recording an overall decreased subscription rate of 63.91% from 94.18% recorded in the previous week.

Summary

Investors continued to show preference to the shorter-term 91-day paper, which can be attributed to investors continuing to see short-term risks in the market. Investor preference to the shorter-term 91-day paper is expected to continue given the rising yields which we expect to cross the 11% level.

EQUITIES

During Q2’2023, the equities market saw a downward trajectory, with NASI, NSE 20, and NSE 25 declining by 5.1%, 2.9% and 8.0%, respectively, taking the H1’2023 performance to losses of 16.0%, 6.0%, and 13.0% for NASI, NSE 20, and NSE 25, respectively.

The equities market poor performance during the quarter was driven by losses recorded by large caps such as KCB Group, Equity Group, and Bamburi of 17.5%, 15.9%, and 10.3%, respectively.

FIXED INCOME SECURITIES – TREASURY BONDS

In the month of June, the government was looking to raise KES 75.00Bn through the issuance of an infrastructure bond – IFB1/2023/007 with a coupon rate of 15.837% and a third tap sale of the FXD1/2023/003 with a coupon rate of 14.228%.

Results

The IFB1/2023/007 was oversubscribed at 367.53%, receiving KES 220.52 Billion worth of bids, out of which the government was seeking to raise KES 60.00 Billion. Out of the KES 220.52 Billion worth of bids received, KES 213.40 Billion worth of bids were accepted. The FXD1/2023/03 was oversubscribed at 123.73%, receiving KES 18.56 Billion worth of bids, out of which the government was seeking to raise KES 15.00 Billion. Out of the KES 18.56 Billion worth of bids received, KES 18.55 Billion worth of bids were accepted.

Summary

The oversubscription came at a time when bonds have been undersubscribed for the past few months, as investors were bidding at higher rates which the government was not willing to borrow at. Additionally, the tax-free nature of the infrastructure bond attracted many investors given the high taxation in the country currently. The impressive coupon rates are a result of market forces as investors continue to seek higher real returns given the rising inflation, which points to the government’s willingness to accommodate higher yields.

What happens when there is a Default Risk?

Bond default payment by the government might occur when the government is experiencing deteriorating conditions that may lead to a decline in revenues, thus making scheduled repayments impossible. This occurs when the tax revenues of the government are no longer enough to cover their debt servicing costs and ongoing expenses.

Solutions to Default Payment

There are a number of ways that the government can solve this problem by restructuring the bond either by lengthening the maturity of the bonds thereby extending the duration or repricing downwards, which implies a haircut on interest.

- Extended Duration

This is the direct conversion of maturing Treasury bills and bonds into longer-term security, which can be offered as a switch bond. Holders of maturing securities are offered a chance to roll over their funds into a longer-term bond with tax incentives and higher coupons to entice them.

This has been recently done, in November 2022, when the Treasury was looking to convert Sh87.8 billion worth of government securities that were due to mature in January 2023 into a medium-term infrastructure bond in order to avoid a cash crunch in January 2023.

CBK was looking to roll over a maturing two-year bond issued in January 2021, from which Sh55.85 billion was due to be repaid to investors. There were also three Treasury bills to be rolled over around the same time in January 2023, comprising a 91-day, 182-day, and 364-day paper with a total value of 31.96 billion.

Holders of these securities were being offered a chance to roll over their funds into a tax-free, 6-year Infrastructure bond, with a coupon rate of 13.215%.

Investors who take up the switch option normally have the added advantage of getting a higher interest rate compared to their maturing holdings.

- Haircut

A haircut refers to the percentage difference between an asset’s market value and the amount that can be used as collateral for a loan.

The government can reduce the value of a bond to restructure the debt to avoid defaulting repayment. For instance, the government can reduce the bond value from the par 100 to 80.

Case in point, in November 2022, Ghana’s government was considering a 30% ‘haircut’ on foreign bonds, and the suspension of interest rate payments to domestic bondholders in 2023 as part of debt restructuring efforts.

FEATURED INVESTMENT SOLUTION

Mansa-X by Standard Investment Bank (SIB)

In Q2’2023, Standard Investment Bank’s (SIB) multi-asset strategy fund Mansa-X (KES Fund) delivered a return of 4.70% with an annualized net return rate of 17.38% (H1’2023).

The USD Mansa-X Fund delivered a return of 2.81% in the same period, with an annualized net returns of 12.38% (H1’2023), continuing to outperform other dollar investment options available locally.

What is Mansa-X?

Mansa-X is a Multi-Asset Strategy Fund with a long/short trading model that invests in local and global financial instruments with the primary objective of realizing capital growth for its investors.

The fund achieves this by utilizing complex portfolio allocation techniques while hedging capital exposure.

Mansa-X exists in both KES & USD options for both local investors and investors in the diaspora.