1. MONEY MARKET FUNDS (MMFs)

The Capital Markets Authority (CMA) released Collective Investment Schemes (CIS) fund performance for 2023. The total assets under management were KES 215,054,231,777 as of December 2023, up from KES 161,004,846,353 as of the end of 2022, signifying a 34% growth year on year.

Money Market Funds (MMFs) accounted for KES. 140.7 billion, which makes up 65% of all the funds under management by Collective Investment Schemes for the quarter that ended December 31, 2023 (source: CMA Website)

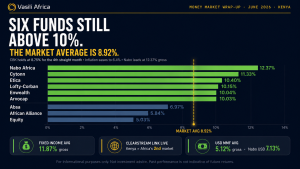

Throughout March, there was a persistent uptrend in money market fund rates, evidenced by the average daily effective rate reaching 13.90% per annum, up from February’s average of 13.37% per annum. The increasing interest rates in Government Securities, a pivotal asset class for money market funds, primarily fueled this escalation.

In terms of individual performance, Etica topped the table with an average daily yield of 16.40% per annum, followed closely by Lofty-Corban, Apollo, Cytonn, and Nabo Africa Money Market Funds, with daily average effective rates of 16.39%, 15.82%, 15.67%, and 15.42% per annum, respectively.

Daily Average Yields for MMFs in March

| NO. | Fund Manager | Name of Fund | AVERAGE (%) |

| 1 | Etica Capital Limited | Etica Money Market Fund | 16.40 |

| 2 | Lofty-Corban | Lofty-Corban Money Market Fund | 16.39 |

| 3 | Apollo Asset Management Company Limited | Apollo Money Market Fund | 15.82 |

| 4 | Cytonn Asset Managers Limited | Cytonn Money Market Fund | 15.67 |

| 5 | Nabo Capital Limited | Nabo Africa Money Market Fund | 15.42 |

| 6 | GenAfrica Asset Managers Limited | GenAfrica Money Market Fund | 15.26 |

| 7 | Enwealth Financial Services | Enwealth Money Market Fund | 14.82 |

| 8 | Kuza Asset Management Limited | Kuza Money Market Fund (KES) | 14.75 |

| 9 | Safaricom Financial Services | Mali Money Market Fund | 14.70 |

| 10 | Madison Investment Managers Limited | Madison Money Market Fund | 14.51 |

| 11 | Jubilee Financial Services Limited | Jubilee Money Market Fund | 14.18 |

| 12 | Co-op Trust Investment Services Limited | Co-op Money Market Fund | 14.03 |

| 13 | KCB Group | KCB Money Market Fund | 13.91 |

| 14 | ABSA Bank | Absa Shilling Fund MMF | 13.88 |

| 15 | Genghis Capital | GenCap Hela Imara Fund | 13.82 |

| 16 | Sanlam Investments East Africa Limited | Sanlam Money Market Fund | 13.62 |

| 17 | African Alliance | African Alliance Kenya Money Market Fund | 13.59 |

| 18 | Mayfair Asset managers | Mayfair Money Market Fund | 12.94 |

| 19 | Dry Associates | Dry Associates Money Market Fund | 12.81 |

| 20 | Old Mutual Investment Group | Old Mutual Money Market Fund | 12.69 |

| 21 | Orient Asset Managers | Orient Kasha Money Market Fund | 12.63 |

| 22 | Equity Bank | Equity Money Market Fund | 12.57 |

| 23 | CIC Asset Managers Limited | CIC Money Market Fund | 12.03 |

| 24 | ICEA Asset Lion Asset Management Limited | ICEA Lion Money Market Fund | 11.58 |

| 25 | Britam Asset Managers (Kenya) Limited | British-American Money Market Fund | 9.56 |

| CUMULATIVE DAILY AVERAGE | 13.90 | ||

Dollar Money Market Fund Returns

In March, Etica MMF USD Fund claimed the top spot with an average return of 7.46%, trailed by Lofty Corban, Cytonn, Kuza, and Dry Associates with average returns of 6.33%, 6.18%, and 5.94%, p.a., respectively.

| NO. | Fund Manager | Name of Fund | AVERAGE (%) |

| 1 | Etica Capital | Etica MMF USD | 7.46 |

| 2 | Lofty-Corban | Lofty-Corban Money Market Fund | 6.33 |

| 3 | Cytonn Asset Managers Limited | Cytonn Money Market Fund | 6.18 |

| 4 | Kuza Asset Management Limited | Kuza Money Market Fund USD | 5.94 |

| 5 | Dry Associates | Dry Associates Money Market Fund | 5.90 |

| 6 | Sanlam Investments East Africa Limited | Sanlam Money Market Fund | 5.85 |

| 7 | Old Mutual Investment Group | Old Mutual Money Market Fund | 5.44 |

| 8 | CIC Asset Managers Limited | CIC Money Market Fund | 5.35 |

| 9 | KCB Group | KCB Money Market Fund | 5.17 |

| 10 | Nabo Capital Limited | Nabo Africa Money Market Fund | 5.03 |

| 11 | ABSA Bank | Absa Shilling Fund MMF | 4.94 |

| CUMULATIVE DAILY AVERAGE | 5.78 | ||

Special Funds and Fixed Income Funds

Lofty Corban Special Money Market Fund secured the leading position with an impressive average return of 16.73%. Madison, Nabo, Kuza, and Zimele Fixed Income Funds followed closely, posting average daily effective returns of 14.38%, 14.30%, 13.26%, and 13.16%, respectively.

| NO. | Fund Manager | Name of Fund | AVERAGE (%) |

| 1 | Lofty Corban Asset Management | Lofty-Corban Special Money Market Fund | 16.73 |

| 2 | Madison Asset Managers | Madison Fixed Income Fund | 14.38 |

| 3 | Nabo Asset Nanagers | Nabo Africa Fixed income Fund | 14.30 |

| 4 | Kuza Asset Management | Kuza Fixed Income Fund (KES) | 13.26 |

| 5 | Zimele Asset Management | Zimele Fixed Income Market Fund | 13.16 |

| 6 | Britam Asset Managers (Kenya) Limited | British Bond Plus Fund | 12.96 |

| 7 | NCBA | NCBA Fixed Income Fund | 12.03 |

| 8 | CIC Asset Managers Limited | CIC Wealth Fund | 11.00 |

| 9 | Orient Asset Management | Orient Hifadhi Fixed Income Fund | 10.85 |

| 10 | African Alliance | African AllianceFixed Income Fund | 10.59 |

| 11 | Mayfair Asset Managers | Mayfair Fixed Income Fund | 10.53 |

| 12 | Sanlam Investments East Africa Limited | Sanlam Fixed Income Fund | 6.86 |

| CUMULATIVE DAILY AVERAGE | 12.22 | ||

2. FIXED INCOME

In March, the government issued 3 fixed-income bonds, comprising two re-openings and one new bond: FXD1/2024/3, FXD1/2023/5, and FXD1/2024/10, respectively in a bid to raise KES. 40Bn through two auctions. The three bonds have terms to maturity of 2.9, 4.4, and 10 years respectively.

The three bonds had different auction dates with FXD1/2024/3 having a coupon rate of 18.38% which consequentially led to a performance rate of 107.7% attributed to the attractive tenor and the coupon. FXD1/2023/5 has a coupon rate of 16.84% and FXD1/2024/10 had a predetermined coupon of 16% signifying the government’s measure to control the bond yields.

Overall, despite high rejection rates of binds received on the 10-year bond, the Government managed to raise about KES 56.8B over and above the targeted amount of KES 40B.

The Government reported an inflation rate of 5.7% for March down from 5.9% in February.

The substantial rejection rate of 79.7% indicates that interest rates may begin to decline, attributable to the government’s decreased reliance on domestic borrowing for funding. This shift could have implications for the stock market, particularly influencing the demand for equities.

As interest rates decrease, investors may turn to equities seeking higher returns, potentially leading to an uptick in their performance. This dynamic reflects the interconnectedness between borrowing rates, government financing strategies, and equity market behavior.

3. EQUITIES

In March, the Kenyan stock market experienced an upward trend, witnessing notable increases in major indexes such as NASI, NSE 25, and NSE 20, which gained 22.3%, 20.2%, and 14.1% respectively. This positive performance in the equities market was predominantly fueled by gains seen in stocks like Safaricom, Equity, and Co-op, which recorded rises of 31%, 18%, and 15% respectively.

BlackRock, one of the globe’s largest asset management firms, made a strategic investment in the Nairobi Securities Exchange (NSE) following a hiatus of four years. This signals a promising trajectory for the NSE and underscores the potential for further growth and development in Kenya’s financial markets.

Foreign investors exhibited a bearish sentiment towards key blue-chip stocks, resulting in a net outflow of USD 1.8 million for the month. The total equity turnover for the month stood at USD 82.9 million, with Safaricom emerging as the most traded counter, accounting for 46% of the overall market activity.

Short-term prospects for the stock market appear uncertain due to the challenging environment and the selling off of assets by foreign investors. However, there is optimism in the long term, driven by low valuations and the potential for both global and local economic recovery.

Additionally, in other news, FY23 Banking sector performance:

- Stanbic Holdings Plc:

- Stanbic achieved a robust FY23 EPS of KES 30.75 with a net income of KES 11.9bn for Stanbic Bank Kenya Ltd.

- It declared a final dividend of KES 14.20 with the book closure being on 17th May 2024. The current price is 130 and the dividend yield is 10.9%.

- Standard Chartered:

- Stanchart posted an impressive FY23 EPS of KES 36.17 with a net income of KES 13.8bn.

- It recommended a final dividend of KES 23.00. The book closure is on 19th April 2024, payment date is on 30th May 2024. The current price is 199.75, with a dividend yield of 14.5%.

- ABSA Bank Kenya Plc:

- Absa achieved solid FY23 EPS growth to KES 3.01 with a net income of KES 16.4bn.

- It proposed a final dividend of KES 1.35 per share. The Book closure is on 30th April 2024, payment date is on 23rd May 2024. The current price is 14.05 with a dividend yield of 12.5%.

- KCB Group Plc:

- KCB experienced a slight decline in FY23 EPS to KES 11.26 with a net income of KES 36.2bn.

- It did not recommend a dividend payment for the year and despite that the current price is at 29.95, up from 24 in March.

- Co-op Bank:

- Recorded a modest increase in FY23 EPS to KES 3.95 with a net income of KES 23.2bn.

- It announced a final dividend of KES 1.50 per share. Book closure is on 29th April 2024, payment date is on 10th June 2024. The current price is 14.95 with a dividend yield of 10%.

- I&M Group Plc:

- Reported a healthy FY23 EPS of KES 7.63 with a net income of KES 12.6bn.

- I&M proposed a final dividend of KES 2.55 per share. Book closure is on 18th April 2024, payment date on 25th May 2024. The current price is 22.10 with a dividend yield of 11.5%.

- Equity Group Plc:

- Witnessed a decrease in FY23 EPS to KES 11.12 with a net income of KES 42.0bn.

- It declared a dividend of KES 4.00 per share. Book closure on 24th May 2024, and payment date on 28th June 2024. The current price is 47 and the dividend yield is 8.5%.

- Equity had a noteworthy balance sheet growth of 25.9% year-on-year.

- NCBA:

- Achieved significant FY23 EPS growth to KES 13.00 with a net income of KES 21.4bn.

- NCBA announced a final dividend of KES 3.00 per share. Book closure is on 30th April 2024, and payment date on 29th May 2024 with a current price of 43.35 and a dividend yield of 11%.

- It demonstrated substantial balance sheet growth of 18.6% year-on-year.

4. GLOBAL MARKETS

In March, the Kenyan shilling has experienced a consistent uptrend, appreciating by 16 percent against the US dollar since the beginning of 2024. This surge in value comes on the heels of the issuance of a $1.5 billion (Sh198.0 billion) Eurobond. The proceeds from this issuance were utilized to partially repurchase the June 2024 $2 billion (Sh264.1 billion) maturity, along with funding the significant oversubscription of the inaugural infrastructure bond issued earlier this year.

Major stock indices had a positive month. The S&P 500 and Nasdaq did particularly well, rising by 3.21% and 1.21%, respectively. Meanwhile, Japan’s Nikkei 225 saw a significant increase of 3.8%, and the UK’s FTSE 100 rose by 4.9%. The Morningstar Global Markets Ex-US index also increased by 3.0%.

The Japan Central Bank made headlines by raising interest rates, marking the end of 8 years of negative rates.

In the US, despite uncertainties surrounding stretched valuations, the upcoming election, and growing debt, rate cuts were postponed due to the economy still showing signs of strength, according to stock market indicators.

March saw energy emerge as the best-performing sector, largely due to favorable oil prices. Bonds also performed positively but with a notable trend: risky assets outpaced quality investments. This trend reflects the resilience of the US economy and signs of recovery in Europe.