1. MONEY MARKET FUNDS

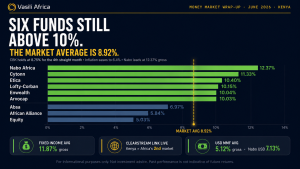

In the month of May 2023, Apollo MMF maintained its position as the best-performing MMF with an average Effective Annual Yield of 10.71%, showcasing an improved performance from the month of April where it recorded an average Effective Annual Yield of 10.49%.

Cytonn MMF and Madison MMF maintained the top 3 position, coming in Second and Third best performing MMFs respectively.

GenAfrica Money Market Fund showcased the highest improvement in performance in the month of May, recording an average Effective Annual Yield of 10.00% as compared to 9.11% recorded in April.

| FUND MANAGER | MONEY MARKET FUND | ANNUAL YIELD % | |

| 1 | Apollo Asset Management Company Limited | Apollo Money Market Fund | 10.71 |

| 2 | Cytonn Asset Managers Limited | Cytonn Money Market Fund | 10.55 |

| 3 | Madison Investment Managers Limited | Madison Money Market Fund | 10.31 |

| 4 | Jubilee Financial Services Limited | Jubilee Money Market Fund | 10.10 |

| 5 | GenAfrica Asset Managers Limited | GenAfrica Money Market Fund | 10.00 |

| 6 | Old Mutual Investment Group | Old Mutual Money Market Fund | 9.69 |

| 7 | African Alliance | African Alliance Kenya Money Market Fund | 9.64 |

| 8 | Kuza Asset Management Limited | Kuza Money Market Fund (KES) | 9.58 |

| 9 | Zimele Asset Management | Zimele Money Market Fund | 9.57 |

| 10 | Sanlam Investments East Africa Limited | Sanlam Money Market Fund | 9.57 |

2. FIXED-INCOME SECURITIES

TREASURY BONDS

In the month of May, the government was looking to raise KES 30.00Bn through two tap-sale issues of the FXD1/2023/003. Additionally, CBK issued IFB1/2023/007 in the last week of May, seeking to raise KES. 60Billion for funding of infrastructure projects in the FY 2022/2023 budget estimates.

(a) TAP SALE – FXD1/2023/003

CBK opened a Tap Sale for FXD1/2023/003, in an aim to raise KES. 10Billion. The coupon rate is 14.228%.

Particulars of the Bonds

| Name | Duration (years) | Coupon Rate |

| FXD1/2023/003 | 3 | 14.228% |

Results:

The tap sale issue for FXD1/2023/003 was oversubscribed at 106.03%, receiving KES 10.603 billion worth of bids, out of the intended KES 10 billion.

(b) SECOND TAP SALE – FXD1/2023/003

CBK opened a Second Tap Sale for FXD1/2023/003, in an aim to raise KES. 20Billion. The coupon rate is 14.228%.

Particulars of the Bonds

| Name | Duration (years) | Coupon Rate |

| FXD1/2023/003 | 3 | 14.228% |

Results:

The tap sale issue for FXD1/2023/003 was oversubscribed at 136.03%, receiving KES 27.206 billion worth of bids, out of the intended KES 20 billion.

(c) IFB1/2023/007

CBK has issued a 7-year Bond seeking to raise KES. 60 Billion for funding of infrastructure projects in the FY 2022/2023 budget estimates.

The period of sale was between 26/05/2023 to 13/06/2023. The Auction date for the IFB1/2023/007 is on 14/06/2023.

Particulars of the Bonds

| Name | Duration (years) | Coupon Rate |

| IFB1/2023/007 | 7 | Market Determined |

● The minimum amount an investor can invest is KES. 100,000.

● The infrastructure bond will be tax-free.

● Redemption date:

- 15th June, 2026 – 20% of unencumbered outstanding principal amount.

- 13th December, 2027 – 30% of unencumbered outstanding principal amount.

- 10th June, 2030 – 100%, final redemption of all outstanding amounts.

An unencumbered outstanding principal amount is the remaining amount of the original loan that is free from claims or doesn’t have any legal right against it.

This means that if an investor has KES 1 Million in full, that is not under lien, they are able to get the 20% of it on 15th June,2026, 30% of it on 13th December, 2027 and the remaining 50% in full at the amortization date (10th June, 2030).

On the other hand, if an investor has pledged the IFB as collateral or if it’s under lien it will not be partially redeemed.

Summary

We attribute the oversubscription to investors continuing to see the market’s short-term risks, hence the high appetite for shorter dated papers. Additionally, investors have been attracted with the high yield and coupon rate that came in at 14.23%, which points to the government’s willingness to accommodate higher yields.

TREASURY BILLS

WEEK 1 – 05/05/2023

T-bills were oversubscribed recording an increased overall subscription rate of 110.72% from 37.52% recorded the previous week.

WEEK 2 – 12/05/2023

T-bills were oversubscribed for the second week recording an increased overall subscription rate of 188.91% from 110.72% recorded the previous week.

WEEK 3 – 19/05/2023

T-bills were oversubscribed for the third week recording a decreased overall subscription rate of 150.09% from 188.91% recorded the previous week.

WEEK 4 – 26/05/2023

T-bills were undersubscribed recording a decreased overall subscription rate of 91.87% from 150.09% recorded the previous week.

Summary

Investors continued to show preference to the shorter-term 91-day paper, which can be attributed to investors continuing to see short-term risks in the market. Investor preference to the shorter-term 91-day paper is expected to continue given the rising yields which we expect to cross the 11% level.

3. EQUITIES

During the month of May, the equities market was on a downward trend with NASI, NSE 20 and NSE 25 declining by 3.7%, 2.0% and 6.7% respectively over the month of May. The poor performance in the equities market was mainly driven by losses recorded by large cap stocks such as Equity Group, Diamond Trust Bank (DTB-K), BAT, Cooperative Bank, NCBA and ABSA Bank of 17.2%, 16.5%, 14.4%, 9.0%, 8.9% and 6.6%, respectively. Despite this, some large cap counters recorded gains such as Standard Chartered Bank of Kenya (SCBK) and Bamburi of 6.9% and 4.8% respectively.

4. REAL ESTATE INVESTMENT TRUSTS (REITS)

The ILAM Fahari I-REIT which is listed on the Nairobi Securities Exchange closed the week trading at an average price of KES 6.0 per share. The performance represented a 4.9% increase from KES 5.8 per share recorded the previous week. Additionally, the performance represented a 69.8% Inception-to-Date (ITD) loss from the KES 20.0 price.

The ILAM Fahari I-REIT currently offers a dividend yield of 10.8%.

5. FEATURED INVESTMENT SOLUTION

PENSION SCHEMES AND MEDICAL INSURANCE

PENSION SCHEMES

NSSF

The National Social Security Fund (NSSF) was established to provide social security to the members of state by increasing the membership coverage of the social security scheme and improving the adequacy of benefits paid out to the scheme by the Fund.

The pensionable age is 60 years, and 50 years is considered as the early retirement age. The pension fund benefits take the form of a retirement pension, an invalidity pension, a survivor’s benefit, a funeral grant and an emigration benefit. The Provident Fund benefits include an age benefit, survivor’s benefit, invalidity benefit and an emigration benefit.

The NSSF is normally exempt from the Stamp Duty Act and the Income Tax Act. Contributions to the Pension Fund form part of tax-deductible expenses in computation of taxes.

NSSF Contributions

The Contributions are categorised into two:

- Tier I contributions – are based on pensionable earnings up to the Lower Earning Limit (LEL)

- Tier II contributions – are based on the difference between the Upper Earning Limit (UEL) and the LEL. The LEL and UEL for the first year of implementation shall be 6,000 and 18,000 respectively as illustrated:

| LEL | UEL | Tier I | Tier II | Total | ||

| 6,000 | 18,000 | Employee | Employer | Employee | Employer | |

| 6% (6,000) | 6% (12,000) | 360 | 360 | 720 | 720 | |

| 720 | 1440 | 2160 |

PENSIONS

A Pension Plan is an investment vehicle, whereby there is a Fund Manager who takes the monthly contributions from employers and employees, and invests the funds with a goal of providing a lumpsum or periodic payments after the beneficiaries retire from employment.

Pension schemes operate through contribution of funds daily, monthly, or even once and upon maturity. The beneficiary is then paid a lump sum or on a monthly basis after retirement or death. The minimum period required for one to be eligible for a pension is at least ten years.

There are two types of pension schemes in Kenya:

- The Individual Pension Plan – the beneficiary makes the contributions personally whether or not he is employed.

When choosing an Individual Personal Pension (IPP) scheme, there are a number of factors that you should consider e.g.:

(a) Security/stability of the company where your IPP is housed.

(b) Longevity of brand – remember your Pension is a long-term financial vehicle so you want to go with a brand that you can have an assurance that even in another 20 / 30 years they will still be on their feet and in business.

(c) Performance and rate of return. You want to review the performance of your pension every few years and you should ensure that you are getting maximum value. Your pension plan is portable and you can always transfer your benefits from one provider to another.

(d) Minimum guaranteed return. IPP schemes guarantee you a minimum rate of return. This means that even in very harsh economic seasons and investment environments, your IPP will not give you a return of less than X%.

- The Occupational Pension Plan – employers contribute on behalf of their employees by deducting the amounts from their monthly salaries. There are two types of Occupational Pensions plans; The Defined Contribution Plan and The Defined Benefit Plan.

Pension schemes are regulated in Kenya by the Retirement Benefits Authority, after satisfactorily fulfilling all requirements.

Pension Schemes in Kenya

1. Jubilee Kenya personal pension plan.

2. KCB pension scheme

3. Boresha Maisha Retirement Plan

4. Britam pension scheme

5. Mbao pension scheme Kenya

6. Zimela’s personal pension plan

7. Kenya Orient Life Assurance Pension

8. Madison Life Assurance Personal Pension Plan

9. Octagon pension services limited.

10. Chancery’s personal pension plan

Benefits of a Pension Plan

(a) Tax Benefit – For the beneficiary to enjoy the tax benefit, the Pension plan needs to be registered under the Retirement Benefit Authority. A beneficiary can get up to KES 20,000 or 30% of their gross salary (whichever is less) tax exempt when contributing to a pension plan. This means that the amount contributed whether KES 20,000 or 30% of the salary will not be taxed.

(b) Security for Mortgage Financing – In Kenya, one can use up to 60% of the retirement savings as security for a mortgage of a primary residence.

(c) Tax-deductible contributions – You can receive tax relief of up to KES 20,000 or KES 240,000 per annum if you contribute to a registered pension scheme. For example, if you earn Ksh. 85,000 per month but save 15% of your salary in a pension scheme, your taxable income is KES 72,250

(d) You pay no tax when transferring your savings from one pension scheme to another.

(e) The first KES 600,000 is tax-exempt for lump sum withdrawals upon retirement.

(f) Upon retirement, your monthly pension is tax-free unless it’s more than KES 25,000 per month or KES 300,000 per year.

(g) You can use up to 60% of your retirement savings as security for your mortgage.

MEDICAL INSURANCE

NHIF

The National Hospital Insurance Fund (NHIF) is a medical insurance provider run by the Government of Kenya. Every employee in Kenya is required to contribute to the NHIF. The Fund’s core mandate is to provide medical insurance cover to all its members and their declared dependants (spouse and children).

The NHIF membership is open to all Kenyans who have attained the age of 18 years. However, one should have a monthly income of more than KES 1,000. NHIF has a presence in the 47 Huduma Centres across the country.

NHIF Contributions

The contributions are segmented, with the maximum contribution currently being KES 1,700 per employee for employees earning more than KES 100,000 per month. The lowest contribution shall be KES 150 for incomes up to KES 5,999.

| Employee’s monthly gross income (KES) | NHIF rates per month (KES) |

| 0 – 5,999 | 150 |

| 6,000 – 7,999 | 300 |

| 8,000 – 11,999 | 400 |

| 12,000 – 14,999 | 500 |

| 15,000 – 19,999 | 600 |

| 20,000 – 24,999 | 750 |

| 25,000 – 29,999 | 850 |

| 30,000 – 34,999 | 900 |

| 35,000 – 39,999 | 950 |

| 40,000 – 44,999 | 1,000 |

| 45,000 – 49,999 | 1,100 |

| 50,000 – 59,999 | 1,200 |

| 60,000 – 69,999 | 1,300 |

| 70,000 – 79,999 | 1,400 |

| 80,000 – 89,999 | 1,500 |

| 90,000 – 99,000 | 1,600 |

| 100,000 and above | 1,700 |

Features

(a) Age – Anyone from the age of 18 years and above, with a National Identity card can take a NHIF cover.

(b) Dependants – With NHIF, there is no limit in the number of dependants one can have. Addition of dependants comes at no additional cost. The age limit for the dependants is 21, school going up to 25. There is no age limit for dependants with disabilities.

(c) Scope of cover – With NHIF one can access outpatient services, inpatient services and maternity for declared spouse. Others services such as optical services or dental services, group life cover and last expense cover are for civil servants and disciplined services members only.

(d) Hospitals – NHIF accredited hospitals are in three categories:

- Category A (government hospitals) – members can enjoy full and comprehensive cover for medical, surgical and maternity services.

- Category B (private mission hospitals) – members may be required to co-pay for where surgery is required.

- Category C (private hospitals) – NHIF pays a specified daily limit and the member is required to up the rest.

(e) Exclusions – NHIF does not cover cosmetic surgery and fertility treatments. Additionally, it doesn’t cover vaccines other than those in the KEPI schedule, anti-rabies, anti-snake venom vaccines and yellow fever.

PRIVATE MEDICAL INSURANCE COVERS

Private health insurance covers are offered by private medical insurance companies in Kenya such as:

1. Jubilee Insurance

2. Madison Insurance

3. Resolution Insurance

4. APA Insurance

5. UAP Insurance

6. Pacis Insurance Company

7. AAR Insurance

8. Britam

9. Heritage Insurance

10. Pan Africa Life

11. Kenindia Assurance Company

Features

(a) Age – Any person between 18 years and 65 years is eligible for an insurance cover for most insurance companies.

(b) Dependants – There are additional premiums for each dependant, spouse and children added. Employers sometimes limit the number of dependants to one spouse plus 3 to 4 children. The age limit for children is 18, and 25years for those who are still schooling.

(c) Scope of cover – Members can only access services as per the premiums they choose to pay. The more the services the higher the premiums. Premiums are normally paid for the different covers:

- Outpatient

- Inpatient

- Maternity

- Optical and dental

(d) Premiums – The premiums paid fully depend on the covers purchased and number of dependants. The rate of the premiums paid tend to increase with age. If an individual is taking their cover for the first time at older age, they tend to pay more in premiums than their younger counterparts for the same type of cover due to their risk profile associated with their age.

(e) Hospitals – Many private hospitals and mission hospitals accept the private health insurance covers. If a member spends more than the specified limit then they are required to top up the extra amount. Payments are usually net of NHIF.

(f) Limits – There is a maximum amount per cover that a member should not exceed within a certain period.

*****

Are you interested in investing in any of these funds? We can help you analyze each further, align with your personal financial plan, and kick off your investment journey.

To get started, contact us via https://vasiliafrica.com/wealth/#call, or call +254 741 808 463.