In our previous article, we dwelled on a very common question on saving, and explained Why your money loses value when you save it in cash. . We also made a recommendation for money market funds as one of the alternatives to saving your money, citing the opportunity to get attractive returns that are way above prevailing inflation rates.

Our article picks up from the last piece, dwelling at length on money market funds, why they are a smart investment option, discuss the type of risk involved, if any then close with the types of money market funds you can consider when you decide to make the decision to start your investment journey.

A. What is a money market fund?

A money market fund in the simplest form is a safe place to park your money and earn an interest higher than that of a bank deposit. It is a type of collective investment scheme that allows investors to pool their resources and invest in low risk, liquid short term debt that provide higher returns. Examples of short term debt include: Treasury bills that are offered by the government, certificates of deposits and short duration corporate debt. Liquidity simply refers to how easy it is to convert the investment into cash.

The goal of money market funds is to seek stability and security by not losing your principal investment. The largest difference between a money market fund and a bank deposit is the ability of the yields (rate earned on the money market) to rise proportionately with interest rates. An example is when interest rates in the Country rise the yield on most bank deposits stays the same while that of a money market fund increases.

Some of the reasons that make money market funds the ideal investment vehicle include:

1. Liquidity- Money market funds do not have a set shelf life and can be liquidated on-demand when the cash is needed. They have a ‘lock up period’ of less than 30 days. A lock up period is the time one is not allowed to withdraw from the fund.

2. Short Term Maturity-The investments done by the fund managers have tenors of 365 days and less

3. Low minimum investment which can be as low Ksh.100

4. Safety- Money Market funds provide a fixed return with short maturities

5. The participants in the market are professional institutions that have their reputations riding on the ability to earn higher returns while still maintaining the safety for investors

B. Why Money Market Fund?

They are an effective addition to an investment portfolio that is in need of high liquidity with a low tolerance of losses. It is a good place to hold cash and earn some interest as you wait to accumulate the money needed for an upcoming purchase or payment you are anticipating.

A good example of when to choose a money market fund is when you have saved enough down payment for your car and you are waiting for the perfect one. Investing in the stock market will be risky because of the market volatility that could eat into your principal investment. Instead of having the money lying around in a savings account you’d rather have it earn the higher interest in the fund.

C. Is a money market fund completely risk-free?

The risks in a money market fund are generally low but this does not mean that they are riskless. Certain events can put pressure on a money market fund, for example, sudden shifts in interest rates or increased withdrawals that were not anticipated. Some of these events could cause the fund to be illiquid and unable to pay back the investors.

To reduce these risks and protect yourself, investors should consider the following:

• Return is directly related with risk- The highest return will most likely be the riskiest. In a bid to increase your return without increasing your risk you can look for funds that have lower management fees.

• Always try and understand what you are getting yourself into by understanding what the fund is composed of. If you are unable to understand look for another fund

D. Which Money Market Fund?

A good money market fund is one that will offer a combination of low risk, high yield and low fees.

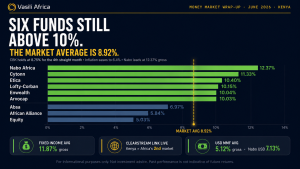

The five best money market funds in the Kenyan market are shown below (sorted by their daily yield).

This article was written by Caroline Musau, Chief Operating Officer at Vasili Africa.

Get in touch with Caroline for free investment advice via info@vasiliafrica.com or fill in your details below.