1. MONEY MARKET FUNDS

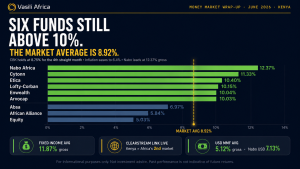

In the month of April 2023, Apollo MMF was the best-performing MMF with an average effective annual yield of 10.49% as compared to March where the best-performing MMF was Cytonn with an average Effective Annual Yield of 10.99%.

Cytonn MMF and Madison MMF maintained in the top 3 positions, coming in as second and third best-performing MMFs respectively.

| FUND MANAGER | MONEY MARKET FUND | AVG EFFECTIVE DAILY YIELD % | |

| 1 | Apollo Asset Management Company Limited | Apollo Money Market Fund | 10.49 |

| 2 | Cytonn Asset Managers Limited | Cytonn Money Market Fund | 10.46 |

| 3 | Madison Investment Managers Limited | Madison Money Market Fund | 9.96 |

| 4 | Jubilee Financial Services Limited | Jubilee Money Market Fund | 9.88 |

| 5 | Kuza Asset Management Limited | Kuza Money Market Fund (KES) | 9.58 |

| 6 | Zimele Asset Management | Zimele Money Market Fund | 9.56 |

| 7 | Nabo Capital Limited | Nabo Africa Money Market Fund | 9.52 |

| 8 | Old Mutual Investment Group | Old Mutual Money Market Fund | 9.46 |

| 9 | African Alliance | African Alliance Kenya Money Market Fund | 9.41 |

| 10 | Sanlam Investments East Africa Limited | Sanlam Money Market Fund | 9.36 |

2. FIXED-INCOME SECURITIES

TREASURY BONDS

In the month of April, the government was looking to raise KES 50.00Bn for budgetary support through a dual issue reopening of three bonds.

(a) FXD2/2018/10

CBK issued a re-opened 10-year fixed coupon treasury Bond seeking to raise KES. 20 billion from the market for Budgetary support.

Particulars of the Bonds

| Name | Duration (years) | Coupon Rate |

| FXD2/2018/10 | 10 | 12.502% |

- The minimum investment is KES. 50,000.

Results

The FXD2/2018/10 was undersubscribed at 17.85%, receiving KES 3.57 billion worth of bids compared to the KES 20 million that the government was looking to raise.

(b) SECOND TAP SALE – IFB1/2023/17

CBK opened a Second Tap Sale for the Infrastructure bond IFB1/2023/17, in an aim to raise KES. 10Billion. The coupon rate is 14.399%.

Particulars of the Bonds

| Name | Duration (years) | Coupon Rate |

| IFB1/2023/17 | 17 | 14.399% |

- The minimum investment is KES. 100,000.

Results

The tap sale issue for IFB1/2023/17 was undersubscribed at 99.96%, receiving KES 5.119 billion worth of bids, out of which KES 5.117 billion were accepted.

(c) FXD1/2022/03 & FXD1/2019/15

CBK issued re-opened 3-year and 15-year 17-year Bonds seeking to raise KES. 30 billion from the market. The period of sale was between 16/03/2023 to 18/04/2023. The Auction date for the FXD1/2022/03 was 19/04/2023.

The Auction for the FXD1/2019/15 was cancelled.

Particulars of the Bonds

| Name | Duration (years) | Coupon Rate |

| FXD1/2022/03 | 3 | 11.766% |

| FXD1/2019/15 | 15 | 12.857% |

- The minimum investment is KES. 50,000.

Results

The FXD1/2022/03 was undersubscribed at 24.43%, receiving KES 7.33 billion worth of bids, out of which KES 1.76 billion were accepted.

(d) FXD1/2023/003

CBK issued a new 3-year fixed coupon treasury Bond seeking to raise KES. 20 billion from the market for Budgetary support. The period of sale is between 26/04/2023 to 09/05/2023.

Particulars of the Bond

| Name | Duration | Coupon Rate |

| FXD1/2023/003 | 3 Years | Market Determined |

- Interest is subject to a withholding tax rate of 15%.

- The minimum investment is KES. 50,000.

TREASURY BILLS

WEEK 1 – 03/04/2023

T-bills were undersubscribed recording a reduced overall subscription rate of 34.42% from 49.16% recorded in the previous week.

WEEK 2 – 11/04/2023

T-bills were oversubscribed recording an increased overall subscription rate of 134.76% from 34.42% recorded in the previous week.

WEEK 3 – 17/04/2023

T-bills were oversubscribed recording a lower overall subscription rate of 122.59% from 134.76% recorded the previous week.

WEEK 4 – 24/04/2023

T-bills were oversubscribed for the third week recording a higher overall subscription rate of 146.47% from 122.59% recorded the previous week.

Summary

The under-subscription in bonds in the last month is mainly because investors bid for higher coupon rates than what the Government was willing to give hence a lot of bids were rejected. In addition, investors are also wary of locking investments in long durations in anticipation of changing interest rates to curb inflation.

3. EQUITIES

During the month of April, the equities market was on a downward trend. The NASI, NSE 20, and NSE 25 declined by 4.5%, 2.7%, and 3.7% respectively over the month of April. The poor performance in the equities market was driven by losses recorded by large-cap stocks such as Bamburi, Standard Chartered Bank of Kenya (SCBK), Safaricom, KCB Group, and EABL of 14.3%, 12.4%, 8.8%, 7.5% and 6.6%, respectively. Despite some shedding, some counters recorded overall gains during the month such as NCBA Group, Diamond Trust Bank Kenya (DTB-K), and BAT of 7.6%, 6.8%, and 1.3% respectively.

4. REAL ESTATE INVESTMENT TRUSTS (REITS)

The ILAM Fahari I-REIT which is listed on the Nairobi Securities Exchange closed the last week of April, trading at an average price of KES 6.1 per share. The performance was a 0.8% gain from KES 6.0 per share recorded the previous week. Additionally, the price performance represents a 69.6% Inception-to-Date (ITD) loss from the KES 20.0 inception price.

The ILAM Fahari I-REIT currently offers a dividend yield of 10.7%.

Acorn D-REIT and I-REIT, which are listed on the NSE traded at KES 23.9 and KES 20.9 per unit, respectively, as of 28th April 2023. The performance represented a 19.4% and 4.4% gain for the D-REIT and IREIT, respectively, from the KES. 20.0 inception price.

5. FEATURED INVESTMENT SOLUTION

SACCOS

A SACCO is a Savings and Credit Co-Operative Society that is member-based and functions like a financial institution owned and controlled by its members.

How to Invest in SACCOS in Kenya

1. Fill out the application/membership joining form

Ask for the application or membership joining from the SACCO you want to invest in and fill it out.

2. Submit the necessary documents

The needed documents are the ID and a copy of your KRA pin. The documents are submitted together with the application form.

3. Pay the joining fee

Depending on the SACCO, pay the joining or registration fee, which is about KES 500 – KES 2,000.

4. Wait for approval to start saving

If you register in person, the approval is usually immediate. Online applications may take around a day or so.

5. Make minimum monthly contributions

Now that you are a registered member, make at least the minimum monthly contribution.

Considerations before joining a SACCO.

a) SASRA Approval

Only go for SACCO Societies Regulatory Authority (SASRA)-approved SACCOS. SASRA guarantees protection from exploitation by SACCOS and investment loss. Once there’s an issue, you can raise it with SASRA, and they’ll pick it up.

SASRA also allows you to identify SACCOS that have collapsed in Kenya, such as the Kiambu Hustlers SACCO and Moi University SACCO, and stay off.

b) Membership Requirements

Consider a SACCO with members with the same interest as you. For example, if you are a business person, consider a business-leaning SACCO and if you are a farmer consider a farmer SACCO if you are into farming.

Then consider the registration requirements, such as the joining fee and the minimum contributions.

c) Dividend Payouts

Dividends are usually calculated as percentages from members’ savings. In Kenya, most SACCOS pay a 10% dividend on average, so the higher the rate, the more the higher the income.

d) Share Capital

Share Capital is the amount that allows SACCO members to have equity ownership and earn dividends annually.

Share capital is not withdrawable but can be transferred or sold during exit.

e) Product Accessibility

Products offered by a SACCO can include credit and savings. Some SACCOS even sell land such as Kimisitu SACCO, Stima SACCO, Kenya Police SACCO, Afya SACCO, or KMA SACCO. Your SACCO of choice should make credit access and savings easy.

f) Customer Reviews and Referrals

Make a point to read customer reviews and ask for referrals from people you know with regard to SACCOS to choose from in order to avoid scamming.

g) SACCO’s Reputation

It is important to choose a SACCO with a proven record. So, consider those that enjoy a good reputation among their customers. Identify the well-established SACCOs.

h) Technology Use

Consider SACCOs which use mobile and internet banking innovations, so that you don’t have to bodily wait in line to be served at a SACCO branch and ensure easy access to their services at any time. Other SACCOs offer ATMs.

i) Payment Tenure

One of the biggest advantages of SACCOs is that they offer longer loan terms. So, if you plan to borrow once you are eligible, you should get a SACCO that offers more extended repayment periods.

j) Customer Service and Location

You want a SACCO you can quickly reach when you have a concern. So, good customer support is critical, which you can tell from the referrals and reviews you read. Choose a SACCO that you can easily access when you want to make an in-person loan request or withdrawal.

k) Exiting Policy

It is advisable to know the exit policy beforehand in case you want to exit the SACCO at some point. Some details in the exit policy include information on what happens to your share capital when you want to opt out.

| Pros of Investing in a SACCO | Cons of Investing in a SACCO |

| Create a Savings culture; A Sacco encourages you to be consistent and have the discipline to save. | Lack of privacy when borrowing; you have to be guaranteed by members of the same Sacco when borrowing with a minimum of 3 members mostly. |

| Access to Emergency Loans like school fees and development loans usually processed within 48 hours of application. | Limited resources: SACCOs can only lend when they have the liquidity to, unlike banks that might have unlimited resources to lend. |

| High Returns: Inform of Dividends on the share capital at the end of the financial year. | Collateral when borrowing; Some SACCOs require you to deposit an asset as security for a loan and in case of default, they can recover the loan through the asset. |

| Access to Credit: SACCOs normally give loans up to 3 times your savings and the interest rates of borrowing are as low as 8% on a reducing balance while bank loans are at 14%+ | Lack of flexibility: When it comes to SACCOS, you have to contribute a minimum amount pre-described per month.

In case of withdrawing from the Sacco, you have to do a total withdrawal and it takes up to 90 days. |

| Long-term Savings: SACCOS are ideal investment vehicles for long-term durations. | Risk of Poor Management: Some SACCOS have been poorly managed in the past leaving members with losses. |

Conclusion;

SACCOs are best suited for people investing in long-term goals. They can help you get the discipline to save since you contribute a minimum amount monthly. Additionally, you can reinvest the interests and dividends you earn. If you are looking at huge borrowing for a project and minimal monthly payments, SACCOs are a good investment product consideration.

Some of the Best Performing SACCOS as of April 2023

| SACCO NAME | YEAR FOUNDED | BRANCHES | MEMBERSHIP | SAVING DIVIDENDS RATE | SHARE CAPITAL DIVIDEND | BEST DEAL |

| Tower Sacco | 1976 | Ol-Kalou (Nyandarua), Nairobi, Nakuru, Nyahururu and Laikipia | 13% | 20% | 16.5 | |

| Hazina Sacco | 1971 | Nairobi | 10.30% | 20% | 15.15 | |

| Police Sacco | 1972 | Nairobi, Eldoret, Kakamega, Nyeri, Kisii, Nakuru, Meru and Mombasa | 60,000 | 10.50% | 17.00% | 13.75% |

| Gusii Mwalimu | 1977 | Kisii, Nyamira Branch,Rongo Branch,

Kilgoris Branch Keroka Branch, Ogembo Branch, |

31,000 | 12% | 13% | 12.5 |

| Sheria Sacco | 8.50% | 16% | 12.25 | |||

| Stima Sacco | 1974 | Nairobi, Mombasa, Kisumu, Nakuru, Ol-Kalou, Eldoret, Embu | 140,000 | 10.30% | 14% | 12.15 |

| Mhasibu Sacco | 1986 | Nairobi, Kisumu, Mombasa | 18,000 | 8.15% | 15% | 11.575 |

| Kimitsu Sacco | 1985 | Nairobi | 9,000 | 8% | 15% | 11.5 |

| Nation Sacco | 1975 | Nairobi | 5,000 | 8% | 15% | 11.5 |

| Safaricom Sacco | 2001 | Nairobi | 12,000 | 7.50% | 12% | 9.6 |

| Finnlemm Sacco | 1997 | Nairobi | 6.20% | 12% | 9.1 |

*****

Are you interested in investing in any of these funds? We can help you analyze each further, align with your personal financial plan, and kick off your investment journey.

To get started, contact us via https://vasiliafrica.com/wealth/#call, or call +254 741 808 463.