1. MONEY MARKET FUNDS (MMFs)

Why do we track the Daily Effective Yield in Money Market Funds?

Money market funds commonly disclose both the daily and annual effective yield. The daily yield signifies the interest earned within a day, while the annual effective yield represents the total return on investment over a year, considering compound interest, assuming all factors remain constant. This metric demonstrates the annual growth rate of an investment, incorporating both interest and compounding effects. Essentially, the earnings on your MMF savings accumulate based on the daily yield, which is compounded monthly.

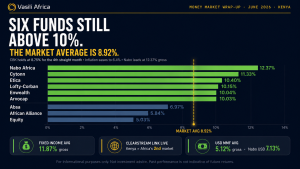

In April, there was a persistent uptrend in money market fund rates, evidenced by the average daily effective rate reaching 14.11% p.a., up from March’s average of 13.90% p.a.

In terms of individual performance, Lofty Corban Money Market Fund topped the table with an average daily yield of 16.84% p.a., followed by Etica, Apollo, Cytonn, and GenAfrica Money Market Funds, with daily average effective rates of 16.70%, 15.94%, 15.79%, and 15.69% p.a., respectively.

Daily Average Yields for MMFs in April

| NO. | FUND MANAGER | FUND NAME | DAILY AVERAGE YIELD (%) |

| 1 | Lofty-Corban | Lofty-Corban Money Market Fund | 16.84 |

| 2 | Etica Capital Limited | Etica Money Market Fund | 16.70 |

| 3 | Apollo Asset Management Company Limited | Apollo Money Market Fund | 15.94 |

| 4 | Cytonn Asset Managers Limited | Cytonn Money Market Fund | 15.79 |

| 5 | GenAfrica Asset Managers Limited | GenAfrica Money Market Fund | 15.69 |

| 6 | Nabo Capital Limited | Nabo Africa Money Market Fund | 15.51 |

| 7 | Kuza Asset Management Limited | Kuza Money Market Fund (KES) | 15.14 |

| 8 | Enwealth Financial Services | Enwealth Money Market Fund | 15.09 |

| 9 | Madison Investment Managers Limited | Madison Money Market Fund | 14.61 |

| 10 | KCB Group | KCB Money Market Fund | 14.48 |

| 11 | Co-op Trust Investment Services Limited | Co-op Money Market Fund | 14.39 |

| 12 | ABSA Bank | Absa Shilling Fund MMF | 14.36 |

| 13 | Jubilee Financial Services Limited | Jubilee Money Market Fund | 14.33 |

| 14 | Sanlam Investments East Africa Limited | Sanlam Money Market Fund | 14.05 |

| 15 | Genghis Capital | GenCap Hela Imara Fund | 14.01 |

| 16 | African Alliance | African Alliance Kenya Money Market Fund | 13.86 |

| 17 | Mayfair Asset managers | Mayfair Money Market Fund | 13.44 |

| 18 | Safaricom Financial Services | Mali Money Market Fund | 13.28 |

| 19 | Equity Bank | Equity Money Market Fund | 13.19 |

| 20 | Dry Associates | Dry Associates Money Market Fund | 12.88 |

| 21 | Old Mutual Investment Group | Old Mutual Money Market Fund | 12.83 |

| 22 | Orient Asset Managers | Orient Kasha Money Market Fund | 12.70 |

| 23 | CIC Asset Managers Limited | CIC Money Market Fund | 12.50 |

| 24 | ICEA Asset Lion Asset Management Limited | ICEA Lion Money Market Fund | 11.62 |

| 25 | Britam Asset Managers (Kenya) Limited | British-American Money Market Fund | 9.46 |

| Average Cumulative Daily Yield | 14.11 | ||

Dollar Money Market Fund Returns

In April, Etica MMF USD fund claimed the top spot with an average return of 7.53%, followed by Lofty Corban, Cytonn, Dry Associates and Kuza MMF USD with daily average returns of 6.38%, 6.07%, and 6.01%, p.a., respectively.

| NO. | FUND MANAGER | FUND NAME | DAILY AVERAGE YIELD (%) |

| 1 | Etica Capital Limited | Etica MMF USD | 7.53 |

| 2 | Lofty-Corban | Lofty-Corban Money Market Fund | 6.38 |

| 3 | Cytonn Asset Managers Limited | Cytonn Money Market Fund | 6.07 |

| 4 | Dry Associates | Dry Associates Money Market Fund | 6.01 |

| 5 | Kuza Asset Management Limited | Kuza Money Market Fund USD | 5.86 |

| 6 | Sanlam Investments East Africa Limited | Sanlam Money Market Fund | 5.86 |

| 7 | Old Mutual Investment Group | Old Mutual Money Market Fund | 5.81 |

| 8 | CIC Asset Managers Limited | CIC Money Market Fund | 5.34 |

| 9 | Nabo Capital Limited | Nabo Africa Money Market Fund | 5.17 |

| 10 | KCB Group | KCB Money Market Fund | 5.08 |

| 11 | ABSA Bank | Absa Dollar Fund MMF | 4.89 |

| Average Cumulative Daily Yield | 5.82 | ||

Special Funds and Fixed Income Funds

Lofty Corban Special Money Market Fund had an impressive return of 16.84%. Madison, Nabo, Kuza, and Zimele Fixed Income Funds posted average daily effective returns of 14.90%, 14.30%, 13.51%, and 13.43%, respectively.

| NO. | FUND MANAGER | FUND NAME | DAILY AVERAGE YIELD (%) |

| 1 | Lofty Corban Asset Management | Lofty-Corban Special Money Market Fund | 16.84 |

| 2 | Madison Asset Managers | Madison Fixed Income Fund | 14.90 |

| 3 | Nabo Asset Nanagers | Nabo Africa Fixed income Fund | 14.30 |

| 4 | Kuza Asset Management | Kuza Fixed Income Fund (KES) | 13.51 |

| 5 | Zimele Asset Management | Zimele Fixed Income Market Fund | 13.43 |

| 6 | Britam Asset Managers (Kenya) Limited | British Bond Plus Fund | 12.72 |

| 7 | NCBA | NCBA Fixed Income Fund | 11.90 |

| 8 | CIC Asset Managers Limited | CIC Wealth Fund | 11.00 |

| 9 | Mayfair Asset Managers | Mayfair Fixed Income Fund | 10.65 |

| 10 | Orient Asset Management | Orient Hifadhi Fixed Income Fund | 10.62 |

| 11 | African Alliance | African AllianceFixed Income Fund | 10.51 |

| 12 | Sanlam Investments East Africa Limited | Sanlam Fixed Income Fund | 6.57 |

The Difference between Money Market Funds and Fixed Income Funds

We generally encounter a fund manager offering both a Money Market Fund (MMF) and a Fixed Income Fund (FIF). The two funds primarily invest in similar types of assets, such as bank deposits, Government securities, and commercial papers, but a way to differentiate the two is how they are administratively structured.

Money market funds (MMFs) are designed for short-term investment, with investments typically having an average maturity of 13 months or less, as regulated. This shorter investment horizon ensures liquidity and stability. On the other hand, FIFs can have longer investment horizons, with securities that may mature beyond the 13-month mark. They typically have more flexibility in terms of the maturity and types of securities they can invest in, depending on the fund’s investment objectives and strategy.

MMFs are often favored by investors seeking capital preservation and liquidity, such as those looking for a safe place to park cash reserves or seeking a stable return in the short term, while FIFs may appeal to investors with longer investment horizons and a willingness to accept slightly higher levels of risk in exchange for potentially higher returns.

2. Fixed Income

In April, the Central Bank of Kenya (CBK) invited bids to raise KES. 40Bn through the re-opening of FXD1/2023/2 with a coupon rate of 16.97%. This is the third time the bond has been re-opened and has a remaining tenor of 1.4 years. The offer attracted bids worth 47 billion, and only 34.7 billion were accepted out of the total received.

The high rejection rate is a signal to investors that interest rates have peaked and are now trending downward.

The government further reopened FXD1/2024/10, a 10-year bond first issued in March 2024 with a coupon rate of 16%, to raise an additional 25B. The bond was undersubscribed, with a total of 14.9 billion bids received, marking a performance rate of 59.9%.

There was a notable decrease in Treasury Bills yields in April. Treasury Bills are often considered a benchmark for short-term interest rates and the decline may serve as a signal that interest rates are on a downward trajectory. A decrease in Treasury Bill yields will likely lead to lower returns for money market funds, which typically invest in low-risk, short-term securities like Treasury Bills. Consequently, investors in these funds may experience diminished yields on their investments during this period of declining rates.

The government reported an inflation rate of 5.0% for April, down from 5.7% in March.

3. Equities

In April, the Kenyan stock market faced a downward trend, marked by significant decreases in major indexes such as NASI, NSE 25, and NSE 20, which saw declines of 5.8%, 4.2%, and 3.5%, respectively. This negative performance was largely driven by losses in key stocks like Co-op, Stanchart, and Safaricom, which experienced drops of 17%, 15.3%, and 10%, respectively.

However, there were notable gains in some large-cap stocks, like EABL, which surged by 22.2%, and Bamburi, which saw a modest increase of 2.1%.

Foreign investors displayed a bullish sentiment towards select blue-chip stocks, resulting in a net inflow of USD 8.0 million for the month. Safaricom emerged as the most traded counter, representing 46% of the overall market activity, contributing to a total equity turnover of USD 55.8 million.

While short-term prospects for the stock market remain uncertain due to prevailing challenges and the divestment of assets by foreign investors, there is optimism for the long term. This optimism is driven by attractive low valuations and the potential for both global and local economic recovery.

Additionally, in other news:

a) Diamond Trust Bank Kenya Ltd (DTB)

- FY23 results: EPS up 13.5% to KES 24.60, net income KES 6.9 billion.

- Revenue: Net Interest Income up 20.5%, Non-Interest Revenue up 34.3%, and total revenue KES 39.7 billion (+24.4%). However, interest expenses grew faster than income, impacting profitability. Operating costs surged due to branch expansion and digital investments.

- Positive: Improved net interest margins, higher dividend payout, increased return on equity.

- Negative: Worsened cost-to-income ratio, declining liquidity ratio.

- Outlook: Positive; agency banking and custody businesses are expected to boost revenue.

- The bank recommended a higher dividend of KES 6.00 per share.

b) Bamburi Cement Plc

- FY23: Per-share loss of KES 0.21, attributed to losses from discontinued operations in Uganda.

- Profit from continuing operations increased.

- Revenue: 6.3% growth driven by higher volume and better pricing.

- Operating profits rose, but expenses increased due to higher freight and electricity tariffs.

- Dividend: Higher at KES 5.47 per share.

- Optimism for special dividend from discontinued operations in Uganda in FY24.

4. Global Markets

In April, major stock indices had a challenging month overall. The S&P 500 and Nasdaq experienced declines of 4.1% and 4.4%, respectively, marking a negative trend. Notably, only the Utilities sector showed positive performance during this period.

Among the remaining sectors, Real Estate took the hardest hit with an 8.5% decline, followed by Technology and Health Care, which fell by 5.8% and 5.0%, respectively. In contrast, the UK FTSE 100 saw a significant uptick of 2.7%, while the Nikkei 225 experienced a downturn of 3.51%.

April emphasized the ongoing concern of persistent inflation, posing a potential threat to the upward momentum of risky assets.

Consequently, it’s crucial to maintain a balanced approach to risk management, considering both the possibilities of recession and deflation, as well as persistent inflation. Investing in high-quality bonds with medium to slightly longer maturities could serve as a buffer, potentially boosting portfolio returns in the event of a deflationary growth shock.