1. MONEY MARKETS

In Q1, the CMA approved three additional unit trust schemes: the Stanbic Unit Trust Scheme, the Taifa Unit Trust Scheme, and the My Xeno Unit Trust Scheme.

Additionally, in May, the CMA approved the Arvocap Unit Trust Scheme, which includes 10 sub-funds: Money Market Fund, Ngao Fixed Income Distribution Fund, Almasi Fixed Income Accumulation Fund, Eurofix Fixed Income Special Fund (USD), Thamani Equity Fund, Africa Equity Special Fund, Global Equity Special Fund, Multi-Asset Strategy Special Fund (USD), Global Sharia Equity Special Fund (USD), and Mabruk Sharia Special Fund (KES).

Furthermore, the CMA approved new sub-funds within existing unit trust schemes, including the Old Mutual Special Fixed Income Fund, NCBA Global Equity Special Fund, NCBA Global Fixed Income Special Fund, KCB Wealth Fund (Special Fund), Jubilee Money Market Fund (USD), and Jubilee Enhanced Fixed-Income Special Fund.

a) Money Market Funds

In the Q1 Collective Investment Schemes report by the Capital Markets Authority (CMA), money market funds’ Assets Under Management (AUM) grew by 6%, rising from Kshs. 140 billion in December 2023 to Kshs. 148 billion in March 2024.

This growth is driven by the introduction of new market entrants who are gaining traction and the digitization of financial products, which have made investing more accessible and convenient, attracting a broader and more tech-savvy investor base.

Hongera to Lofty Corban and Kuza Money Market Funds, who reached KES 1 billion AUM milestone!

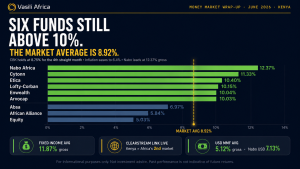

There has been a consistent upward trend in money market fund rates, with the average daily effective rate increasing to 14.16% p.a., up from April’s average of 14.11% p.a.

Lofty Corban Money Market Fund topped the table with an average daily yield of 16.94% p.a., followed by Etica, Cytonn, Apollo, and Kuza Money Market Funds, with daily average effective rates of 16.65%, 15.94%, 15.92%, and 15.52% p.a., respectively.

Daily Average Yields for MMFs in May

| NO. | FUND MANAGER | FUND NAME | Daily Average Yield (%) |

| 1 | Lofty-Corban | Lofty-Corban Money Market Fund | 16.94 |

| 2 | Etica Capital Limited | Etica Money Market Fund | 16.65 |

| 3 | Cytonn Asset Managers Limited | Cytonn Money Market Fund | 15.94 |

| 4 | Apollo Asset Management Company Limited | Apollo Money Market Fund | 15.92 |

| 5 | Kuza Asset Management Limited | Kuza Money Market Fund (KES) | 15.52 |

| 6 | GenAfrica Asset Managers Limited | GenAfrica Money Market Fund | 15.40 |

| 7 | Nabo Capital Limited | Nabo Money Market Fund | 15.27 |

| 8 | Enwealth Financial Services | Enwealth Money Market Fund | 14.94 |

| 9 | Madison Investment Managers Limited | Madison Money Market Fund | 14.55 |

| 10 | KCB Group | KCB Money Market Fund | 14.49 |

| 11 | Jubilee Financial Services Limited | Jubilee Money Market Fund | 14.44 |

| 12 | Co-op Trust Investment Services Limited | Co-op Money Market Fund | 14.40 |

| 13 | ABSA Bank | Absa Shilling Fund MMF | 14.28 |

| 14 | Genghis Capital | GenCap Hela Imara Fund | 14.24 |

| 15 | Sanlam Investments East Africa Limited | Sanlam Money Market Fund | 14.09 |

| 16 | Mayfair Asset managers | Mayfair Money Market Fund | 13.99 |

| 17 | African Alliance | African Alliance Kenya Money Market Fund | 13.86 |

| 18 | Dry Associates | Dry Associates Money Market Fund | 13.09 |

| 19 | Equity Bank | Equity Money Market Fund | 12.86 |

| 20 | Orient Asset Managers | Orient Kasha Money Market Fund | 12.78 |

| 21 | Old Mutual Investment Group | Old Mutual Money Market Fund | 12.67 |

| 22 | CIC Asset Managers Limited | CIC Money Market Fund | 12.50 |

| 23 | ICEA Asset Lion Asset Management Limited | ICEA Lion Money Market Fund | 11.58 |

| 24 | Britam Asset Managers (Kenya) Limited | British-American Money Market Fund | 9.52 |

| CUMULATIVE DAILY AVERAGE (%) | 14.16 | ||

b) Dollar Money Market Fund Returns

Etica MMF USD fund claimed the top spot with an average return of 7.04%, followed by Lofty Corban, Dry Associates, Kuza, and Sanlam MMF USD with daily average returns of 6.38%, 6.25%, 6.20%, and 6.13%, p.a., respectively.

| NO. | FUND MANAGER | FUND NAME | DAILY AVERAGE YIELD (%) |

| 1 | Etica Capital Limited | Etica MMF USD | 7.04 |

| 2 | Lofty-Corban | Lofty-Corban Money Market Fund | 6.38 |

| 3 | Dry Associates | Dry Associates Money Market Fund | 6.25 |

| 4 | Kuza Asset Management Limited | Kuza Money Market Fund USD | 6.20 |

| 5 | Sanlam Investments East Africa Limited | Sanlam Money Market Fund | 6.13 |

| 6 | Old Mutual Investment Group | Old Mutual Money Market Fund | 5.87 |

| 7 | KCB Group | KCB Money Market Fund | 5.36 |

| 8 | CIC Asset Managers Limited | CIC Money Market Fund | 5.19 |

| 9 | ABSA Bank | Absa Dollar Fund MMF | 5.16 |

| 10 | Nabo Capital Limited | Nabo Africa Money Market Fund | 4.76 |

| Cumulative Daily Average Yield (%) | 5.83 | ||

c) Special Funds and Fixed Income Funds

Lofty Corban Special Money Market Fund had an impressive return of 16.84%. Madison, Etica, Kuza, and Nabo Fixed Income Funds posted average daily effective returns of 14.90%, 14.85%, 13.97%, and 13.41%, respectively.

In May, Britam Asset Management introduced 3 fixed-income funds for 3, 6, and 12 months, respectively.

| NO. | FUND MANAGER | FUND NAME | DAILY AVERAGE YIELD (%) |

| 1 | Lofty Corban Asset Management | Lofty-Corban Special Money Market Fund | 16.75 |

| 2 | Madison Asset Managers | Madison Fixed Income Fund | 14.90 |

| 3 | Etica Capital Limited | Etica Fixed Income Fund | 14.85 |

| 4 | Kuza Asset Management | Kuza Fixed Income Fund (KES) | 13.97 |

| 5 | Nabo Africa Managers | Nabo Africa Fixed Income Fund | 13.41 |

| 6 | Zimele Asset Management | Zimele Fixed Income Market Fund | 13.27 |

| 7 | Britam Asset Managers (Kenya) Limited | British Bond Plus Fund | 13.00 |

| 8 | Britam Asset Managers (Kenya) Limited | Britam Special Fixed Income Fund, 1 year | 12.46 |

| 9 | Britam Asset Managers (Kenya) Limited | Britam Special fixed Income Fund, 6 Months | 12.28 |

| 10 | Britam Asset Managers (Kenya) Limited | Britam Special fixed Income Fund, 3 months | 12.26 |

| 11 | NCBA | NCBA Fixed Income Fund | 11.78 |

| 12 | Mayfair Asset Managers | Mayfair Fixed Income Fund | 11.10 |

| 13 | CIC Asset Managers Limited | CIC Wealth Fund | 11.00 |

| 14 | African Alliance | African AllianceFixed Income Fund | 10.71 |

| 15 | Orient Asset Management | Orient Hifadhi Fixed Income Fund | 10.41 |

| 16 | Sanlam Investments East Africa Limited | Sanlam Fixed Income Fund | 6.48 |

2. EQUITIES

In May, the Kenyan stock market experienced an upward trend, marked by significant increases in major indexes such as NASI, NSE 25, and NSE 20, which rose by 6.0%, 3.9%, and 1.9%, respectively.

This positive performance was largely driven by gains in key stocks like KCB, Safaricom, and Stanchart, which surged by 19%, 12%, and 11%, respectively.

However, there were notable losses in some large-cap stocks like Bamburi and Stanbic, which dropped by 14% and 12%, respectively.

Equities turnover for May was USD 138.1 Million, a 148% increase from USD 55.8 million in April. This significant increase in equity turnover indicates heightened trading activity and investor interest in the market.

Foreign investors displayed a bullish sentiment towards select blue-chip stocks, resulting in a net inflow of USD 11.1 million for the month, a 39% increase from the net inflow of USD 8 million in April.

Additionally, in other news:

a) Safaricom Group Performance and Outlook

Safaricom Group reported earnings per share (EPS) of KES 1.57 for FY24, a slight increase from KES 1.55 last year. This growth was due to a 12.4% rise in revenue to KES 349.5 billion and better profit margins as revenues grew faster than costs.

Key highlights include:

- Total Revenue: Reached KES 335.4 billion, up 13.4% from last year.

- M-Pesa Revenue: Increased by 19.5% to KES 140.0 billion, benefiting from the reintroduction of mobile money to bank charges in Kenya.

- Data Revenue: Grew by 22.2% to KES 82.4 billion, with mobile data growing by 24.9% to KES 67.4 billion. Despite lower data prices, more people used mobile data, boosting revenues.

- Voice Revenue: Fell slightly by 0.6% to KES 80.5 billion.

- SMS Revenue: Increased by 8.3% to KES 12.3 billion due to better customer management.

- Costs: Total costs rose by 8.8% to KES 186.2 billion, with operating costs at KES 83.3 billion and direct costs at KES 97.1 billion.

- Profit Before Interest, Tax, Depreciation, and Amortization (EBITDA): Increased by 16.8% to KES 163.3 billion, with improved profit margins.

- After-Tax Profit: Decreased by 18.7% to KES 42.7 billion. Profits in Kenya grew by 14.4% to KES 84.8 billion, while Ethiopia reported a larger loss of KES 42.1 billion compared to last year’s KES 21.6 billion loss.

Outlook:

- Data revenue is expected to continue growing due to more people using 4G and online services.

- Traditional services like voice calls and SMS are likely to face more pressure.

Dividend:

The board recommended a final dividend of KES 0.65 per share, making the total dividend for FY24 KES 1.20, the same as last year. The final dividend will be paid around 31st August 2024 to shareholders recorded by 31st July 2024.

b) Equity Group Plc Performance

Equity Group Plc released its 1Q24 results, showing a strong performance with key highlights as follows:

- Earnings Per Share (EPS): Increased by 25.1% year-on-year to KES 4.08.

- Net Income: Reached KES 16.7 billion.

Key Highlights:

- Equity Bank Kenya: The primary subsidiary saw a 24.0% decline in net income to KES 5.5 billion due to higher costs, including a 67.9% increase in interest expenses to KES 13.3 billion and a 34.5% rise in provisions to KES 2.5 billion.

- Non-Interest Revenue (NIR): Dropped by 25.3% to KES 18.3 billion.

- Net Interest Income (NII): Grew by 7.4% to KES 13.9 billion.

- Total Fees and Commissions: Increased by 22.6% to KES 13.6 billion.

- Trade Finance: Generated KES 3.1 billion, with off-balance sheet facilitation growing by 23% to KES 205.6 billion.

Loan and Revenue Performance:

- Loan Book Growth: Modest at 3.0% year-on-year.

- Interest Income from Loans: Increased by 31.9% to KES 27.3 billion.

- Government Annuities Income: Increased by 36.5%.

- Customer Deposits: Grew by 11.3% to KES 1.2 trillion.

- Interest Expenses: Rose by 41.4% to KES 15.2 billion.

Costs and Transactions:

- Operating Expenses: Rose by 19.7% to KES 23.6 billion.

- Staff Costs: Increased by 17.1%.

- Other Operating Costs: Increased by 21.9% to KES 13.8 billion.

- Mobile Banking Transactions: Decreased by 42% in volume but increased in value by 34% to KES 532.9 billion.

Positives:

Geographical and Product Diversification: 63% of profitability now comes from regional subsidiaries, up from 46%. The Democratic Republic of Congo (DRC) accounts for 28% of profit before tax, compared to Kenya’s 35%.

Negatives:

Equity Bank Kenya: Continued to struggle with a 24% decline in net income due to higher interest expenses and operating costs.

c) Stanbic Bank Kenya Ltd Performance

Stanbic Bank Kenya Ltd, the primary subsidiary of Stanbic Holdings Plc, posted a modest 2.7% increase in 1Q24, with earnings per share (EPS) at KES 10.11 compared to KES 9.84 in 1Q23. Key highlights are as follows:

Key Highlights:

- Net Interest Income (NII): Increased by 19.6% to KES 6.5 billion, driven by a 53.0% rise in income from loans and advances, which totaled KES 9.2 billion. The bank’s loan book grew by 11.7% year-on-year to KES 255.8 billion.

- Non-Interest Revenue (NIR): Declined by 34.0% to KES 3.8 billion, mainly due to a 44.0% drop in foreign exchange income and a 40.1% decrease in fees and commissions from loans and advances.

- Interest Expenses: Grew by 130.2% year-on-year, with expenses related to customer deposits rising 1.7 times to KES 4.9 billion.

Positives:

- Cost to Income Ratio: Improved to 35.7% from 40.1%, thanks to efficiency gains from integrating and automating operations, digitizing customer channels, and optimizing foreign currency contracts.

- Liquidity Ratio: Increased to 51.2% from 45.6% in 1Q23, with deposits and balances due from banking institutions abroad reaching KES 27.8 billion.

Negatives:

Mark-to-Market Losses: Related to government securities increased by 45.3% year-on-year to KES 38.6 million, although the bank reduced its exposure to government securities by 37.2%.

3. GLOBAL MARKETS

United States

- Economy: Solid overall, but showing some signs of slowing in capital spending and home sales.

- Stock Market: Major stock indices saw significant gains: Nasdaq up 8.5%, S&P 500 up 5%, and Dow Jones up 3.3%. Gains were driven primarily by tech stocks, with Nvidia contributing a quarter of the gains in the S&P 500, alongside Apple, Microsoft, and Alphabet. Nvidia saw a 262% jump in sales. The tech sector rose by 10%, utilities by 9%, while energy declined by 0.4% due to falling oil prices.

- Inflation: Yearly rates slowed to 3.4% and 3.6%.

- Interest Rates: No immediate cuts expected; US Treasuries rallied.

Europe

- Economic Activity: Improving with strong performance in the services sector and signs of recovery in manufacturing.

- GDP Growth: 0.3% for the first quarter.

- Stock Market: European stocks (excluding the UK) rose by 3.6%, while UK stocks increased by 2.4%.

- Inflation: Headline inflation at 2.6%, core inflation at 2.9%.

- Interest Rates: The European Central Bank (ECB) is likely to cut rates in June.

Asia

- China: Positive economic data and an equity market rebound, though domestic demand and real estate issues remain weak.

- Japan: The weak yen is hurting consumer sentiment, leading to a modest stock market increase of 1.2%.

- Inflation: Mixed, with core inflation remaining above targets.

Monetary Policy

- United States: Concerns over inflation progress, with no rate cuts expected soon.

- Eurozone: Confident about disinflation, with potential rate cuts on the horizon.

- United Kingdom: High inflation, making rate cuts unlikely in June.

- Japan: Balancing the need to support a weak currency with cautious rate hikes.

Key Economic Trends:

- US Business Spending: Increased in April, with strong business activity in May.

- Eurozone Business Activity: Expanded at the fastest pace in a year in May.

- UK Retail Sales: Fell due to poor weather conditions in April.

- China Retail Sales: Slower growth, but strong industrial production.

- China-US Trade Tensions: China is reducing US bond holdings and increasing gold reserves.

Investment Highlights:

- Government Bonds: Expected to remain volatile but still valuable for income and diversification.

- Credit Spreads: Stable, with strong performance in investment-grade credit and emerging market debt.

- Equity Markets: Mixed global performance, with strong rebounds in the US and Europe, but weaker performance in Japan.